Multiplying An Inheritance and Making It Tax Free

Dan and Joyce have always considered leaving a legacy to be one of their God given duties. They believe the legacy they leave should include:

· A love and respect for their Creator (Proverbs 3:7-8)

· A good name (Proverbs 22:1)

· A joyful and positive spirit (Proverbs 17:22)

· An inheritance for their children and grandchildren (Proverbs 13:22) and,

· The means to continue stewardship over their legacy (Proverbs 22:28).

Legacy has lost much of its significance in modern America. In early American, as in ancient times, a legacy was the way a family made sure it would survive from one generation to the next. Without a legacy, a family could easily become beholden to cruel creditors, corrupt landlords and eventually obliterated. Thus, building a solid, sustainable legacy was not only important it was considered a sign of God’s grace.

This is why Presbyterian officials in Pennsylvania began the Corporation for Relief of Poor and Distressed Widows and Children of Presbyterian Ministers in May of 1759. It was important to the church leaders to establish a means by which continued stewardship of a deceased minister’s family and estate could be sustained.

Other, less scrupulous parties followed suit offering life insurance coverage to the public without having the financial solvency to pay claims when an insured died. This practice, which took advantage of people by charging high premiums without providing any guarantees or lifetime coverage triggered Elizur Wright, an abolitionist, who is often referred to as the Father of Life Insurance. He was as determined to stop these illicit business practices as he was determined to abolish slavery. A brilliant mathematician, Wright constructed actuarial tables detailing how much money an insurance company needed to keep in reserve in order to guarantee payments when a death claim occurred. He also established the first non-forfeiture life insurance policies which defined how much money the insurance company should refund to a policyholder if they surrendered their life insurance while they were still living. In 1858, Wright became Massachusetts’ State Insurance Commissioner, giving him authority to regulate all insurance companies in the state of Massachusetts. Many insurance companies resented and resisted Wright but, in the end, the honest life insurance companies realized Wright’s way of doing things was right. In fact, Wright’s insurance regulations improved the sale of life insurance, making it not only affordable and comfortable for people in all financial classes but something that was desired as well.

It wasn’t long before other states followed Massachusetts’ example and established the same kind of regulatory standards. Today life insurance, especially non-forfeiture life insurance like participating whole life insurance, is one of the safest places to keep and store money to establish and maintain a legacy.

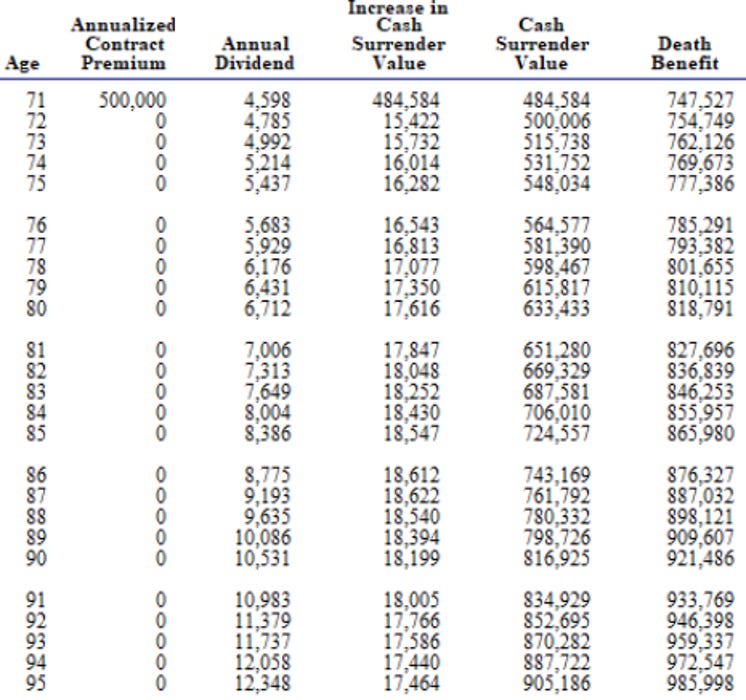

Dan and Joyce realized this and naturally wanted to purchase participating whole life insurance as a way of providing the means of maintaining their legacy. They knew a non-forfeiture life insurance policy would guarantee the provision necessary for their heirs, both children and grandchildren, to sustain and maintain their legacy. Dan and Joyce accomplished this by purchasing a Single Premium Participating Whole Life Insurance Policy (SPPWLIP) with some of the money they realized they were not going to use or need during the remainder of their lifetime.

At age 71, Dan and Joyce spent $500,000 and purchased a SPPWLIP on Dan’s life. This policy provides, that in the event Dan dies, he would immediately multiple his legacy by 49.5%, leaving a tax-free inheritance of $747,527 to his children and grandchildren. If Dan continues to live past age 85, the life expectancy of a healthy 71-year-old male, he will leave an even larger inheritance of $865,980 tax free to his children and grandchildren.

If perchance, Dan and Joyce need extra money in their retirement years, Dan’s SPPWLIP has cash value which is accessible to them. They can either chose to surrender part, or all, of Dan’s death benefit and withdraw the money needed, or they can leverage Dan’s death benefit, use it as collateral, and borrow the money needed from the insurance company. Either way, Dan and Joyce realize that exercising these options, will create an income tax liability for them and less money to sustain and maintain the rest of the legacy they are leaving to their heirs. But because the money used to purchase Dan’s SPPWLIP is something Dan or Joyce are NOT depending on, even if they do need to access extra money in the future from this insurance policy, the income tax will not be something which will be a financial burden for them.

Today, 70% of households won’t leave a financial legacy without life insurance. SPPWLIPs are a way to multiple a financial inheritance, guaranteeing the legacy will be larger than without an SPPWLIP, and that it will be transferred tax free to the heirs. Thanks to the Presbyterians of Pennsylvania and people like Elizur Wright who established non-forfeiture life insurance (participating whole life insurance) making it such a reliable and dependable financial tool which avoids taxes, while multiplying an inheritance, makes sustaining a family legacy a reality for millions of Americans.

At McFie Insurance we design and sale non-forfeiture life insurance policies. SPPWLIP is only one type of non-forfeiture life insurance. There are other types of non-forfeiture life insurance which are more suitable for those who are younger than Dan and Joyce. These types of non-forfeiture life insurance policies can be used by individuals and business owners to recoup the cost of things purchased, which leads to building and growing a larger legacy for you, your children, and your grandchildren. Call us at 317-912-1000 for your no fee, no obligation consultation.