Infinite Banking: Interest Paid or Interest Recovered On Debt

Credit card debt continues to enslave many Americans. According to CBS, 11.12% of credit card accounts are only receiving minimal payments while the average credit card balance has soared to $6,580.

What does it look like to pay minimal payments on a credit card balance of $6,580? Using Consolidated Credit Solutions calculator, where a minimal payment of 3% of the balance is due each month, plus interest (which is 24% on the average credit card in 2025), it will take 284 monthly payments to eliminate $6,580 of credit card debt. This is 23 years and 8 months, with a cost of $12,269.57. This is $5,689.57 more the original $6,580 balance due.

In addition to credit card debt, hundreds of thousands of Americans, 60 years old and older, are still holding $125 billion in students loan debt. Over 190,000 seniors are now subject to having their Social Security benefits garnished to repay this massive amount of student loan debt. All this because the earnings of these individuals never rose to justify their education expenses.

Add to this, we know that more that 1 out of 2 Americans support their parents, forcing them to take early retirement withdrawals incurring additional debt. This is unsustainable for obvious reasons. Yet it is happening. And it forcing 3 out of 10 Americans to retire with less than $100,000 in savings.

Then there is the debt assumed by parents to help their children attend college. According to the Princeton Review 77% of parents cover a portion of their child’s college costs and 18% of parents assume debt in order to do so.

And finally, 23% of parents who are helping their children with college are still paying off their own student loan debts.

Debt, debt and more debt. The question is, “How much of this debt is being recovered by the person who is paying off this debt? Unfortunately, the kind of debt mentioned here is really just a huge transfer of wealth from lower- and middle-class Americans to creditors, as none of it is every recovered.

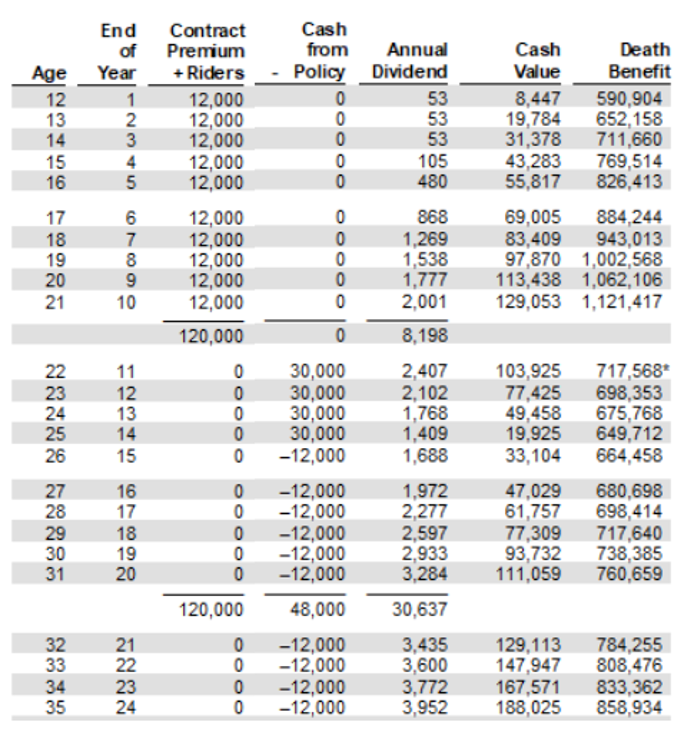

As of 2025, in-state college tuition runs on average at about $11,000 per year and out-of-state tuition runs about $30,000. Xaivera’s parents started saving for her college education when she was 12 years old by putting away $1,000 a month for the next 10 years. When Xaivera enrolled at an out-of-state college, her parents had her covered.

When Xaivera was 21, her parents had $129,053 of cash value in her policy. This allowed them to take $30,000 in policy loans every year for 4 years in a row. During this time, they didn’t pay a dime of interest, premium or make any loan repayments.

After Xaivera graduated from college, both her and her parents repaid the $120,000 of accumulated policy loans they had taken to pay for her college education. They did this by paying $1,000 per month back to the insurance company that issued Xaivera’s policy. In 10 years, when Xaivera turned 35, her entire college student loans, which her parents had taken from her policy, were fully repaid.

At age 35 Xaivera’s policy contained $188,025 of cash value. This is $168,100 more than the $19,925 which was left in cash values after her parents had borrowed $120,000 (4 x $30,000) to pay for her college education.

Between Xaivera’s 12th and 21st years, her parents paid $120,000 in premiums and together her and her parents paid $120,000 in policy loan repayments. Of the total $240,000 paid in premiums and loan repayments they still have $188,025 of cash value PLUS Xaivera’s college degree. This means Xaivera’s college education only cost $51,975, the difference between $240,000 and $188,025.

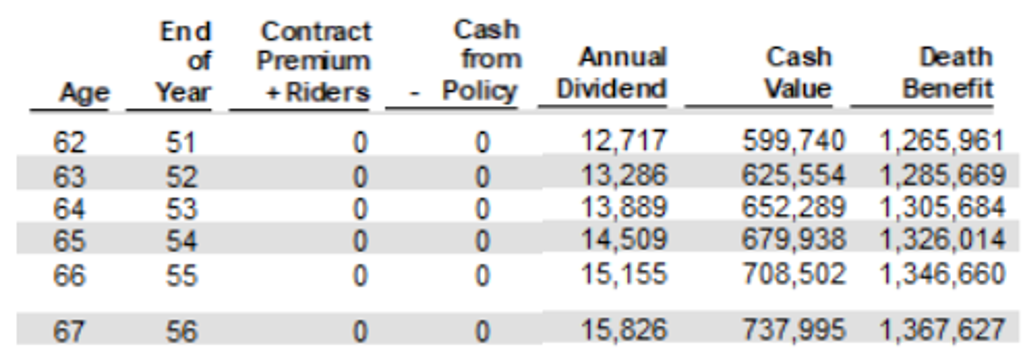

But hold on a moment. At age 67 when Xaivera retires, her participating whole life insurance policy will have $737,995 of cash value even though no further premiums or loan repayments will have been paid into this policy.

The cost of this policy was only $120,000, the other $120,000 paid was for policy loans taken for Xaivera’s college education, which her parents or Xaivera would have had to spend anyway. If that original $120,000 of premium payments had been invested for 46 years (67 years – 21 years), it would have had to earn an average 4.028% after taxes, to match the $737,995 Xaivera’s policy will provide her when she turns 67. When you consider Xaivera can access this $737,995 without taxes or penalties, it makes this participating whole life policy a great tool not only to save but to recover the cost of debt.

As debt is crippling hundreds of thousands of Americans today, participating whole life insurance should be better utilized to avoid the transfer of wealth that is occurring from the lower- and middle-income classes to their creditors.

To see your own customized life insurance illustration call 317-912-1000. To read more about using cash value life insurance to recover the cost of things financed, download the free binder on Infinite Banking Made Simple, available here: https://mcfieinsurance.com/

Tom McFie is the founder of McFie Insurance and co-host of the WealthTalks podcast which helps people keep more of the money they make. He has reviewed 1000s of whole life insurance policies and has practiced the Infinite Banking Concept for nearly 20 years, making him one of the foremost experts on recovering the cost of finance. His latest book, A Biblical Guide to Personal Finance, can be purchased here.