Infinite Banking Blog: What If Wages Were Tied to the Stock Market?

According to the Social Security Administration, the average wage in America increased by 107.19% between 2000 and 2023.

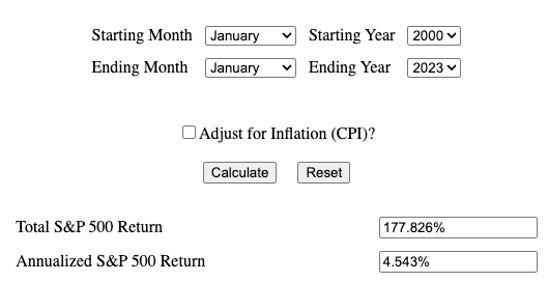

Annualized return on the S&P500 between 2000 to 2023 was 4.543%. This represents a 177.826% total return over 23 years.

If wages were tied to the stock market, average wages would have increased significantly more between 2000 and 2023. However, from 2000 to 2014 the S&P 500 only increased by 27.832% while wages increased by 44.5574%. Thus, for the first 14 years of this time period, wages increased more rapidly than the stock market did.

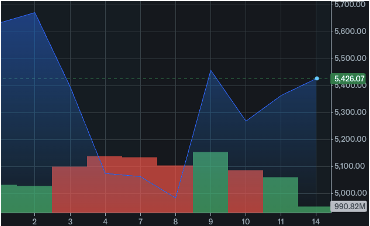

But nobody ever earns what the stock market produces. This is because there are direct, and indirect costs associated with investing. These costs include brokerage charges, taxes, commissions, management fees etc., all of which must be factored in before any gains can can be counted as profits. And until profits are taken, there is always the risk of losing any gains, because of market volatility. Take the attached chart from April 2-14th, 2025, as an example.

So, if wages were tied to the stock market, it would throw a monkey wrench into buying groceries, paying bills or saving for the future when there was a sudden significant drop.

· But if money spent could be recovered and used over again how would that affect your finances?

Recovering the cost of things purchased is the main premise behind Infinite Banking. Consider the following story about a young doctor, whom we will call Jeramy.

1. Jeramy knew he wanted to invest in real estate

2. He began saving $834 a month to make his first investment

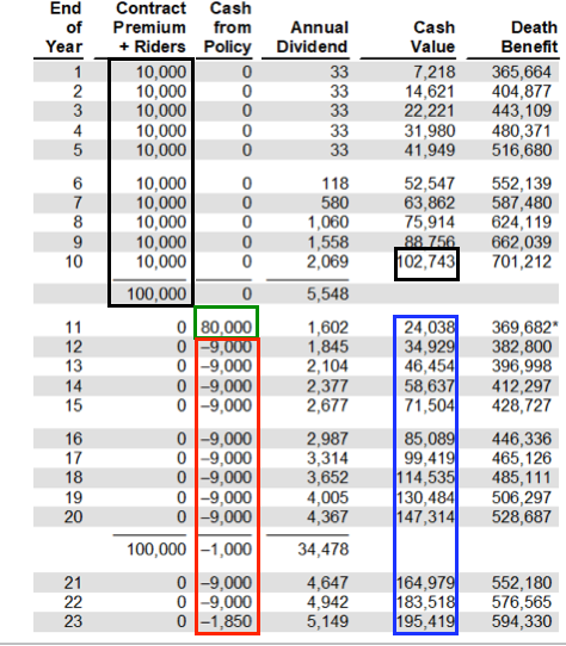

3. He paid $834 every month towards the premium of a participating whole life insurance policy to build cash value AND have the coverage he needed for his family

4. When Jeramy had built $102,743 of cash value in his policy, he used his participating whole life insurance as collateral and borrowed $80,000 from the life insurance company

5. Jeramy used this $80,000 to purchase his first rental property, a mobile home

6. Jeramy’s rental provided him with $750 of cash flow per month or $9,000 annually

7. Jeramy directed this cash flow back to the insurance company repaying his policy loan for a total principal and interest of $100,850

8. After the loan was repaid Jeramy had $195,419 of cash value in his policy

9. This was $171,381 more cash value than what he had after he borrowed the $80,000 from the life insurance company ($24,038 in year 11)

10. Jeramy was able to recover 100% of the $100,850 he repaid on his real estate loan, and

11. His life insurance provided him with an additional $70,531 ($171,381 - $100,850)

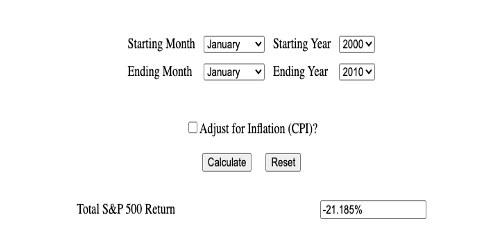

If Jeramy had purchased the S&P 500 with his $834 a month, beginning in January 2000 through January 2010, instead of purchasing his participating whole life policy he would have lost money because the market had a -21.185% return over those 10 years. But when Jeramy used his $834 a month to purchase participating whole life insurance, he built the cash value which allowed him to leverage his policy and use the borrowed $80,000 to make his real estate investment. In doing so, Jeramy experienced a 69.9365% gain over his total loan costs. Imagine earning a return on loan or lease payments.

A traditional $80,000 loan at 5% would have cost Jeramy $739 per month for 12 years, a total of $106,547. His $739 monthly payment would have eaten up all but $11 of cash flow from his rental. Instead, Jeramy recovered 100% of the $100,850 he paid to the insurance company in interest and principal [($9,000 x 11) + $1,850] and has $195,419 of cash value to show for it.

Think about this. Would you rather have your wages tied to the stock market or would you prefer being able to recover the cost of things purchased and profit by doing so?

If Jeramy hadn’t used participating whole life insurance to store his money, he wouldn’t have been able to borrow against it and purchase real estate. Things would have turned out quite differently for him. For example, if Jeramy had parked $834 every month into a savings account, and could have earned 1.5% on that savings, he would have had $107,903 after 10 years. This is $5,160 more than $102,743 of cash value after 10 years. By putting his savings up as collateral to borrow $80,000 @5% for his real estate purchase, Jeramy would have been required to go through underwriting, plus he would have had to pay $739 per month for 12 years, or a total of $106,547, to a bank instead of being able to recover the money he repaid for his policy loan. In the meantime, Jeramy’s savings of $107,903 would have continued to generate 1.5%, producing another $21,266, not $70,531 like his participating whole life insurance policy did, making his total savings just $129,169 instead of the $171,381 cash value his policy generated for him.

For one, I am glad wages are not tied to the stock market. It would merely add more chaos to life due to the volatility of the market. But having money stored up in participating life insurance allows me, as a policyowner, to recover the cost of things purchased, while my policy continues growing, generating better than average returns of any savings plan.

Infinite Banking is a process, which uses a product called participating whole life insurance to enhance profits by allowing the policyholder to keep more of their hard-earned money. With no brokerage charges, taxes, commissions (commissions are paid out of the insurance company’s profits not the policyholder’s premiums), management fees, etc., Infinite Banking is a proven way to generate higher profits whenever you make a purchase, invest, finance or refinance something.

Visit us at McFieInsurance.com or call us at 317-912-1000 to learn more.