Infinite Banking and Policy Dividends

Much goes into a well-designed participating whole life policy which can be used with the Infinite Banking process.

Dividends are one of the hotly disputed items when it comes to policy design. Agents love to wrangle about how their insurance company has been paying dividends for 100 years or more consecutively, or brag about how their insurance company pays higher dividends than another competitive company.

Here the scoop and why most of these disputes are irrelevant.

First of all, dividends are great, if they are paid. But the fact of the matter is, dividends don’t have to be paid. Dividends add value when they are paid but they are not guaranteed to be paid regardless of past history or how large the dividends are projected to be in future years.

Second, even if an agent brags about the high dividends their company is paying it doesn’t mean their company will always pay a higher dividend. There are multiple companies who used to pay great dividends which now no longer pay any dividends. This kind of stuff happens in the real world.

Lastly, even when a dividend is paid which is higher than anther company’s dividend, it doesn’t always translate into greater cash values for the policyholder

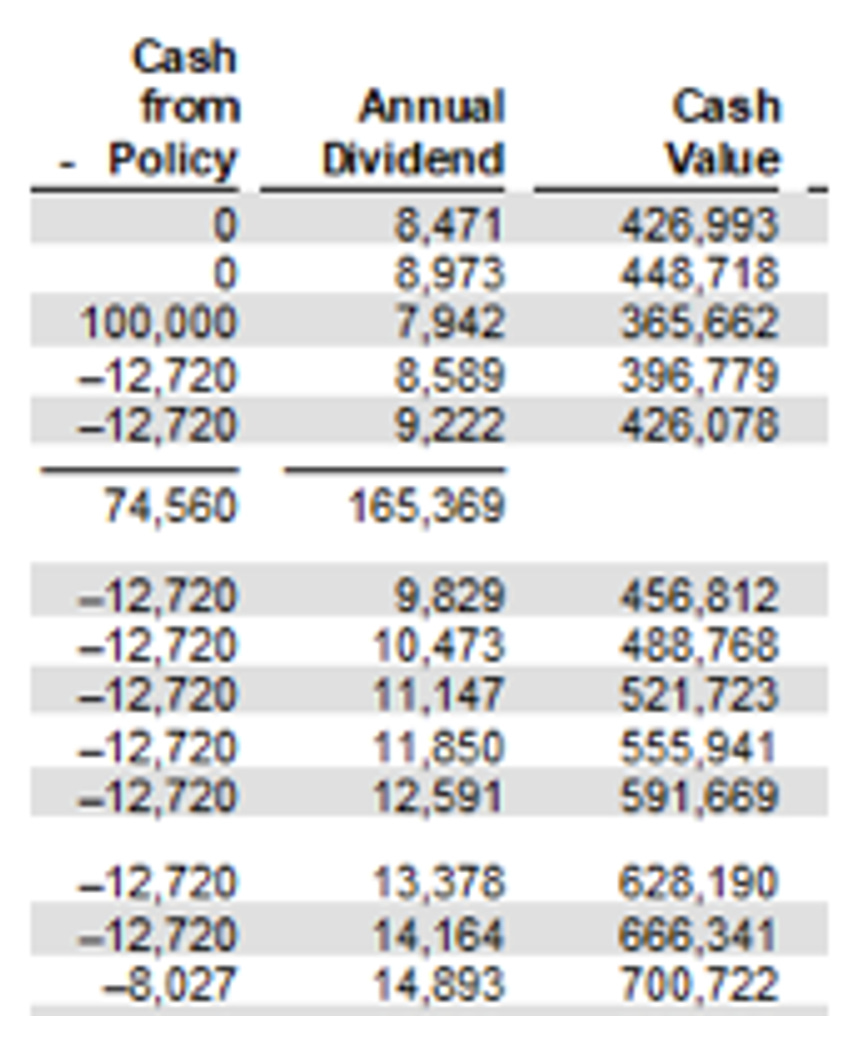

.Consider policy A. The annual dividend is significantly lower than the dividend in policy B. But when comparing the increase in cash value the dividend purchases in policy A, to what the cash value the dividend purchases in policy B, there is a substantial difference.

When policy A’s dividend is $8,973 the cash value gained from this dividend is $21,725 ($448,718 - $426,993), 142.115% more than the dividend payment. In policy B, for the same year with the same premiums having been paid to date as in policy A, the dividend is $18,029 but the cash value gained from this dividend payment is $27,180. This is only 50.757% more than the dividend payment. So much for higher dividends.

With the guaranteed cash value in policy A ringing in at $284,941, and the guaranteed values in policy B ringing in at only $175,121, just $1,282 more than the total amount of premiums paid towards each of these policies it becomes obvious dividends, even when higher, are not the most important part of Infinite Banking.

Dividends are great when they paid but they aren’t guaranteed to be paid. And even when they are paid it doesn’t always translate into producing a dollar-to-dollar increase in cash values.

Ultimately, Infinite Banking boils down to leveraging the guaranteed cash values as a form of collateral without hindering the continued compounding growth of those cash values, and using the borrowed money to finance some purchase like a car, equipment, investments, real estate, vacations, etc. Such policy loans do NOT hinder the guaranteed compounding growth of the cash values giving the policyowner the financial capability of recovering the cost of whatever was purchased with Infinite Banking financing.

So when $100,000 is borrowed against policy A’s cash values and repaid over 10 years (or however many years the policyowner determines) the policyowner ends up recovering everything they pay for this $100,000 loan [($12,720 x 9) + $8,027] = $122,507 and the policy gains $335,060 ($700,722 - $356,662).

This proves that the cost of things purchased, when financed with the Infinite Banking process, can completely be recovered. And in this case, not only is the cost recovered but an additional $212,553 is added to the $122,507 which was recovered ($335,060 - $122,507).

The way people think about things is the way they respond to things. Infinite Banking is a process which puts into practice what banks and lending institutions practice on a daily basis. It isn’t some magical pill or potion to swallow or rub on. It is a powerful way to manage money so that the cost of things purchased is not lost and the compounding growth on money is not transferred to some middleman like a bank or credit card company.

Every investment and purchase in life is financed either by giving up interest which could have been earned on savings when it is spent, or interest and principal is given up when credit is used, this interest and principal is directed back into the account of those who practice Infinite Banking financing.

Building cash values in participating whole life insurance to a point where it is beneficial to leverage and borrow the insurance company’s money, is the major downside of Infinite Banking. But to finance with savings takes time, and repaying a creditor takes time as well, and time will pass by regardless of if the Infinite Banking process is utilized or not. So why not use the time to build the cash value necessary so you can benefit from financing with Infinite Banking? It’s a great way to keep more of the money you earn, and it can pay dividends.