Generating Generational Wealth Via Infinite Banking

According to Education Data Initiative, as of 2024, total student loan debt in America reached $1.77 trillion. This is equivalent to every man, woman and child in America owing $5,057.

In 2024, 53% of undergraduate students who completed their degree, used federal loans to pay for their tuition. In addition, nearly a quarter of all student borrowers had extra debt related to their education on top of their student loans. This extra debt included home equity loans, private loans, credit card balances, and personal lines of credit. This is an insane amount of debt, especially when considering the amount of debt-to-income ratio is 7% for the average college graduate.

Debt is a dirty 4 letter word when creditors control you. According to CNBC, the average interest rate on student loan debt was 7.94% in 2024. The average student loan debt assumed by undergraduate students, according to Business Insider, is $29,300. At 7.94% over ten years it will cost $42,548 to pay off $29,300 of student loan debt.

What would that $42,548 @ 3.5% become if it didn’t have to been expensed out to pay for student loan debt over 10 years? The answer is $50,856.

So how can someone who plans to attend college and earn a degree but also wants to keep that $50,856 themself instead of paying it all to the creditor who provided their student loans? The answer is Infinite Banking.

George the father of an 8-year-old, wants to have at least $100,000 of life insurance for his family and save for his child’s college education. George can easily accomplish this by:

· Purchasing a 10-year term policy for $101 per year and saving $3,499 a year which is compounding at the average 0.42% rate of return earned in most savings accounts. But George realizes he will not have any coverage after 10 years and will have spent $1,010

· So, he spends $300 a month for 10 years, and purchases a $100,000 participating whole life insurance which will provide his family with over $100,000 of coverage for the rest of his life, and help finance his child’s college tuition.

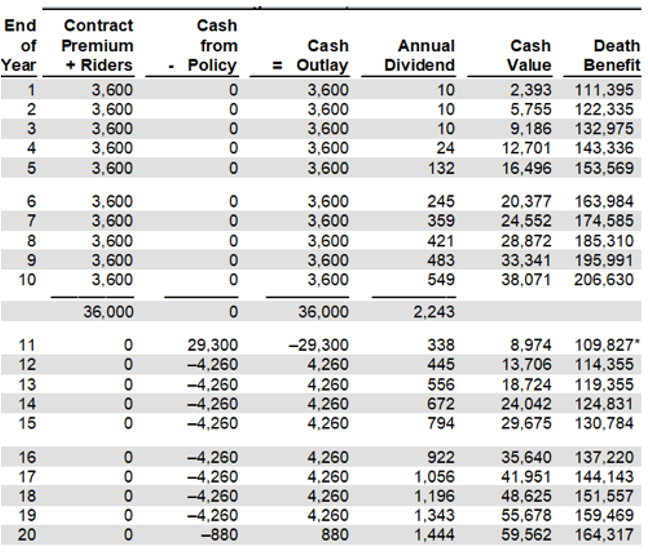

Here’s what happened.

1. George paid $300 a month for 10 years into a participating whole life insurance policy and ended up in year 10 with $38,071 of cash value and $206,630 of coverage for his family.

2. Then he borrowed $29,300 against this policy to pay for his child’s college tuition and still had $109,827 of coverage for his family.

3. Next George repaid the policy loan at, $4,260 per year… about half the rate an average student loan would cost for this same $29,300 balance.

4. After 9 years George had paid $39,220 in repayments (including interest) instead of $42,548 for a savings of $3,328.

5. His cash value grew from $8,974 to $59,562 during those same 10 years for a growth of $50,588

6. $3,328 saved, combined with $50,588 of cash value growth, means George completely recovered the $39,220 it cost him to pay his child’s tuition plus another $14,696 for a total of $53,916.

After repaying this policy “student” loan, George has $164,317 of life insurance coverage which will continue to increase for the rest of his life, without him paying another dime in premiums. He also has $59,562 of cash value which means the original $30,000 he paid for this policy has compounded by 7.099% over the last 10 years, without him owing taxes or spending any more money on premiums.

Most importantly, George, nor his child, were ever in debt where some creditor was calling the shots on when and how much they had to repay for this policy “student” loan. This type of loan is fully collateralized by the insurance policy itself. Thus, if George so desired, he could have paid less and taken longer to repay this policy loan. Or he could have repaid it quicker. But another option George had was, he could have simply turned the policy loan into a partial surrender of his life insurance coverage. This would have reduced his life insurance coverage but would have completely erased the loan and any interest owed.

Options, options, options. Options help to generate wealth and create generational wealth without incurring taxes, fees, penalties or interest paid to creditors. When George passes at or around age 85, which most American men do, he will leave $267,521 from this policy to his heirs, no taxes owed! This seed money can be used to start this entire process over again with his grandchildren or even his great grandchildren.

Perpetual wealth from one generation to the next without transferring the wealth to some third-party creditor. That’s the power of Infinite Banking.

To discover more about Infinite Banking, download the free binder on Infinite Banking Made Simple, available here: https://mcfieinsurance.com/

Tom McFie is the founder of McFie Insurance and co-host of the WealthTalks podcast which helps people keep more of the money they make. He has sold and reviewed 1000s of whole life insurance policies and has practiced the Infinite Banking Concept for nearly 20 years, making him one of the foremost experts on recovering the cost of finance. His latest book, A Biblical Guide to Personal Finance, can be purchased here.