Fertility, Finances, the Future and Participating Whole Life Insurance

The United States has been reproducing at below population replacement levels for nearly 20 years.

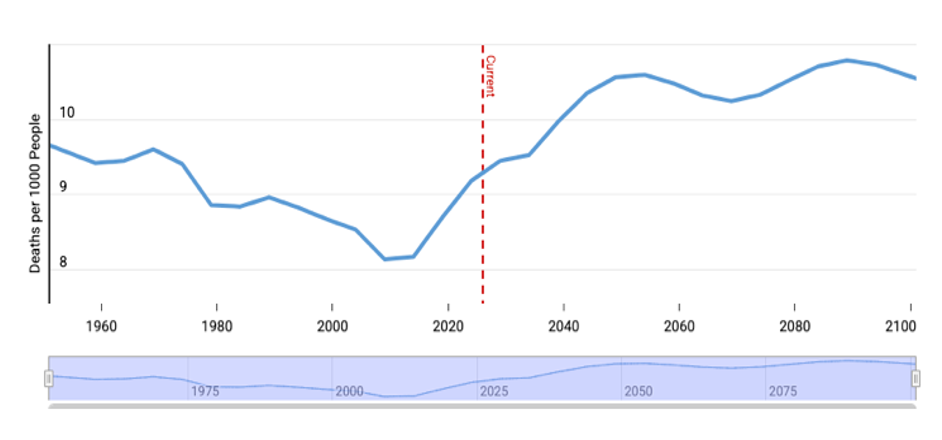

Meanwhile, mortality rates have increased significantly since around 2007 in the United States. And the combination of these two trends doesn’t bode well for the United States long term.

Some models show, beginning in 2033, the US population dramatically declining when the large Boomer population mortality rate climaxes and these lower reproduction rates overlap.

Though environmental issues known to reduce fertility are a concern, these concerns are not the top reason America is not reproducing at a level to sustain itself. The most common factor responsible for the declining fertility rate is finances.

Many couples today have financial anxiety and don’t believe they have the financial means to support children. According to one study, as reported in Nation World, 54% of Americans in 2023 are worried about not having enough money to support a family. Roughly 3.6 million children are born in the United States each year. The birth rate is declining partly because immigration flatlines salaries and drives up housing prices, making it doubly difficult for couples to have all the children they would like. Yet, children are a gift from the Lord: they are a reward from him, Psalm 127:3. Even so, the fear of having children is heightened because of the massive amount of student loan debt and/or consumer debt being carried by so many.

America ushered in 2025 with consumers carrying $1.166 trillion of credit card debt according to LendingTree.com. A recent Bankrate report shows that 48% of Americans carry their credit card debt from month to month. And even though Biden forgave $183.6 billion of student loan debt, 2025 started out with student loan debt exceeding $1.76 trillion. This is a massive amount of debt. No wonder people are fraught with financial anxiety and not wanting to shoulder the financial responsibility of having children.

But it doesn’t have to be this way. There is a beautiful way to resolve financial anxiety, and it isn’t speculation or investing more in your 401(K) or IRA. It is found in the ageless book of Proverbs, which was penned by the wisest, and perhaps the richest, man in history, King Solomon.

In the book of Proverbs, Solomon shares over 130 different facts about money, riches, wealth, prosperity and poverty. And these facts are still applicable. Anybody who is serious about applying them to their own financial situation will find they all still work today just like they did over 3000 years ago when Solomon wrote them down for posterity. With 31 chapters in the book of Proverbs, it makes sense to read at least one chapter daily, to glean all this knowledge, apply it, and reap the benefits while avoiding the pitfalls associated with money and riches.

Stacy was once part of the nearly two trillion-dollar credit card debt in America. She was trapped with credit card debt which exceeded her annual income. And just like 5 out of 10 Americans , she kept rolling the balances from month to month never paying them off. She was in perpetual debt, enslaved to the credit card companies she owed money to, Proverbs 22:7.

When Stacy first heard about the Infinite Banking Concept (IBC), as taught by the McFie Insurance life insurance agents, she realized IBC was a way to eliminate her financial anxiety and gain financial liberty. Stacy began to apply the 10-20-70 principle, limiting her credit card payments to just 20 percent of her monthly income. She reassessed her living expenses and determined she was going to live on 70 percent of her income, which left her with 10 percent of her income to keep for herself. Like Proverbs 16:8 implies, keeping a little of what you earn is better than having more if it causes injustice. And Stacy understood the injustice the 21% plus interest rates were for her and her family. This injustice was killing them financially.

According to the IBC, as taught by McFie Insurance, Stacy used 10 percent of her income to purchase a participating whole life policy on her life. This participating whole life insurance policy initially would have paid off her credit card debt plus provided over $100,000 for her family if she passed before she could pay off her debts. The participating whole life insurance policy also began to develop cash value. This cash value was crucial in helping Stacy eliminate her credit card debt while generating wealth and establish her financial liberty.

This is how it all panned out. Over the next several months after she purchased her participating whole life insurance policy, Stacy leveraged the cash value of her participating whole life insurance policy and used the money to pay off her credit cards as soon as possible. This effectually transferred her credit card debt to her participating whole life insurance policy which had an interest rate of only 5% instead of the credit card interest of 21% and higher.

Repeating this process each time her cash values increased Stacy was able to pay off her credit cards in less than three years. Then she directed the 20% of income she had been paying to the credit card companies back to her life insurance policy. This restored her ability to leverage the repaid cash value again, plus any additional growth, for a future need, investment or emergency.

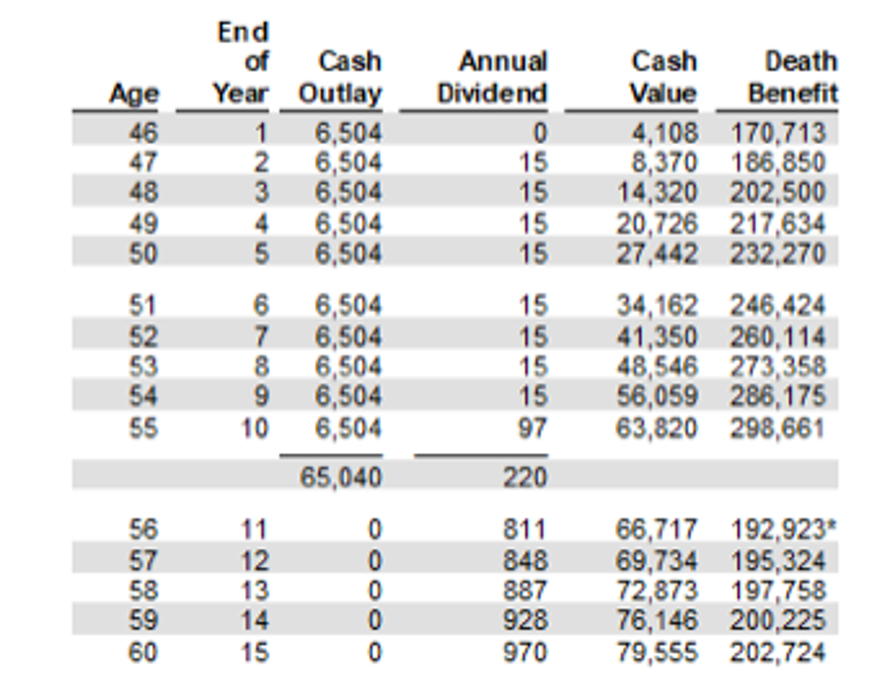

By year five, Stacy had completely repaid the loans she had taken against her policy cash values. The 10% of her income, which she was paying every month for her participating whole life insurance policy, was $542, So for year six, her cash value growth was equivalent to earning 7.104% APR on those $542 monthly premiums for the year, ($34,162 -$27,442 = $6,720). Additionally, her death benefit had grown 44.35% from her initial first year death benefit. Both the cash value and death benefit will continue to increase as long a Stacy is alive even though in year ten, she will have completed the purchase of this participating whole life insurance policy and will never have to pay another dime for it.

It took Stacy five short years to accomplish something she had been trying to accomplish for over 10 years but without any success. Looking back Stacy realizes, her attempt to pay off her credit card debt, without having any reward for doing so, was unsuccessful because she had no objective other than to get out debt. That isn’t a bad objective it just shouldn’t be a first objective. Getting out of debt is an honorable objective but not necessarily a liberating objective. Owning participating whole life insurance gave Stacy a way to measure and quantify her progress as she paid off her credit card debt. It was the difference between night and day. Nobody relishes sacrificing today unless they can be assured of the benefits their sacrifice will provide them tomorrow. Stacy’s participating whole life insurance policy provided the tangible, quantitative benefit she needed to overcome her financial anxiety and accept financial liberty.

Without working longer hours, taking a second job or giving up things which made her life comfortable, Stacy was able to accomplish her objective. In the process she learned to listen and be open to a better way to tackle her debt than what she had been attempting, Proverbs 16:20. In doing so she was able to experience the success and financial liberty she had desired to achieve many years before.

Today Stacy is no longer worried about where the money will come from to support her family or to leave a legacy for her grandchildren, Proverbs 13:22. She knows when she turns 56 she will no longer have to keep directing 10% of her income towards this participating whole life insurance policy. Instead she could direct that money to another participating whole life insurance policy which will increase her resources for the future and accomplish her goal of building a legacy for her children and grandchildren. She also knows that her cash values will continue to grow, until the day she passes, giving her the peace of mind that she can access this money, eliminating a potential financial burden for herself or her family in the future.

It is exciting to see the emotional wealth Stacy has developed throughout this entire process, Proverbs 31:25. She is no longer worried about the future. She acknowledges money gained quickly (credit card debt) can create financial anxiety, but money gained little by little grows, Proverbs 13:11. She also recognizes not having to comply with financial obligations owed to others frees up creativity and allows her to keep more of the money she generates, Proverbs 22:7

Stacy also appreciates the freedom which borrowing against her participating whole life insurance policy provides for her, giving her the financial ability to quickly and efficiently eliminate her credit card debt and freeing her from the terms and conditions of others in regards to payment schedules and interest rates. Finally, Stacy has come to recognize keeping just 10% of her income is only the beginning of what she can accomplish financially with participating whole life insurance. Free from the financial anxiety, which her credit card debt produced, Stacy is now able to be more generous, helping others who are not as fortunate as she is. This is the most gratifying experience Stacy has experienced. And it all comes down to becoming her own banker and applying the financial principles found throughout the book of Proverbs.

Participating whole life insurance is really an American brainchild. It is not available for sale in any other country outside North America. And it was Americans who took the concept of life insurance, as experienced in the old world, and refined it to provide the guaranteed death benefit, the continued cash value growth, the level premium, and the profit sharing (dividend) which participating whole life insurance provides today.

It was these guarantees which led the majority of Americans in the 20th century to purchase participating whole life insurance. Regrettably, the 21st century usured in a disdain for owing participating whole life insurance, thus Americans are not as well prepared to meet the financial obligations of having children, paying off debt, establishing their own financial liberty, owning their own home or even becoming as prosperous as former generations of Americans were. But as Stacy’s testament proves, it doesn’t have to be that way. The rich will always rule over the poor, Proverbs 22:7, but all hard work generates a profit, Proverbs 14:23. And though poverty is still a choice many will choose over being prosperous, the book of Proverbs, which is free for all, remains the best instruction guide for anyone who wants to abandon poverty and appreciate prosperity. Combined with owning participating whole life insurance, the book of Proverbs can help anyone become more prosperous, wealthy and in the position to manage and control more money than they currently are doing.

McFie Insurance is dedicated to helping others apply the truths contained in Proverbs by using participating whole life insurance and other proven financial tools to make you more prosperous and wealthy. You can improve your financial future, keep control over more of the money you generate, and be more generous to family, friends and the needy while designing a brighter future for America and yourself. Call 702-660-7000 to find out more.